Climatetransition 2026

From CO₂ambition to robust strategy

Climate is no longer a separate sustainability issue for companies. It's a factor that directly affects their customer relationships, supply chains, investment decisions, and cost structure.

Perhaps one (or more) of these scenarios is already familiar to you:

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Unordered list

- Item A

- Item B

- Item C

CSRD-rapportage is geen verslag dat je in enkele maanden tijd realiseert. Het is een organisatiebreed proces dat voorbereiding vraagt op vlak van data, governance, processen en strategie - en dat vergt meer tijd dan de meeste organisaties verwachten.

why2026 is a tipping point

Three developments are making climate an essential component of competitive positioning:

1. Transparency is becoming structural

Due to the Corporate Sustainability Reporting Directive (CSRD) and pressure from the financial world, CO2 data is becoming public, comparable, and subject to assurance. Your emissions and reduction trajectory will become visible to customers, banks, investors and competitors. Climate data will thus evolve from an internal reporting tool to an external assessment criterion.

2. Emissions are being priced

Through the ETS system, internal carbon pricing and the CBAM, CO2 is increasingly being translated into concrete costs. These costs have a structural impact on margins and pricing, and also influence investment decisions. CO2 is becoming an economic factor: companies with a higher CO2 intensity will have to bear structurally higher costs than competitors with lower emission profiles.

3. Chain responsibility is shifting upstream

For large customers, scope 3 emissions are decisive in achieving their own targets. This shifts the pressure to the chain.

Climate performance is increasingly becoming adecisive factor in tenders and a criterion for selecting suppliers. You therefore need it to retain customers and enter into strategic partnerships. Those who do not understand their chain impact risk losing market share.

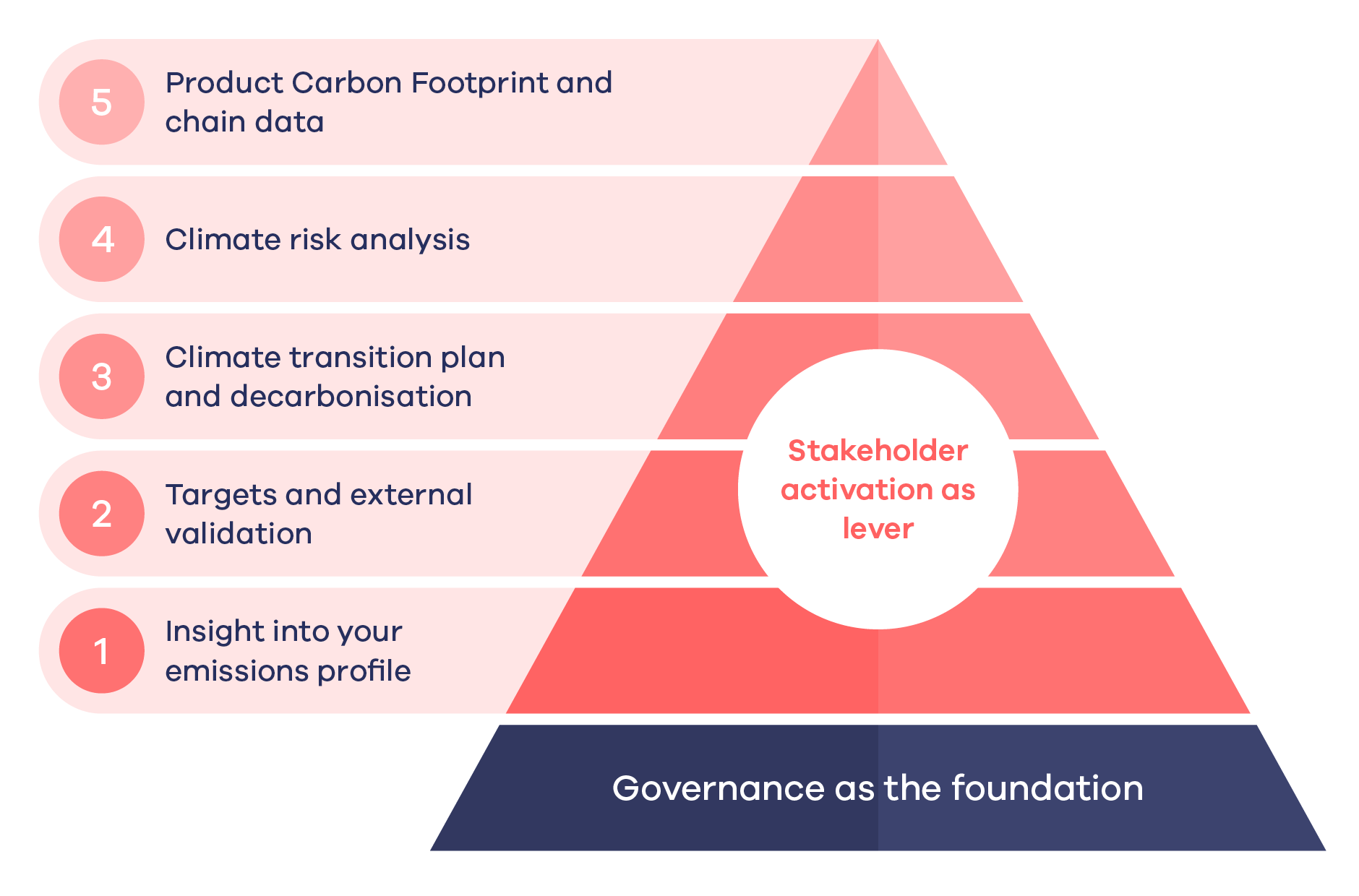

ThePantarein-model

In our work with industrial and internationally active companies, we use an integrated model to structurally embed climate considerations into business operations.

A future-proof approach has five substantive dimensions – from insight into your Corporate Carbon Footprint (CCF) to CO2 at market and product level – and rests on a single foundation: clear governance. Stakeholder engagement forms the outer shell that is relevant across all steps.

Dimension 1: insight into your emissions profile

A robust strategy starts with a clear understanding of your emissions. This means that you:

- identify scope 1, 2 and 3 emissions;

- critically assess the data quality;

- identify emission hotspots;

- distinguish between controllable and structural emissions.

Your CCF is more than just a measurement exercise. It is an analytical tool to understand which emissions are strategically decisive, gain insight into chain dependencies, and translate emissions data into investment priorities.

Dimension 2: targets and external validation

A robust climate strategy requires clear CO2 targets. Clear targets determinethe pace of reduction, guide investment choices, and create internal focus and accountability.

External validation through the Science Based Targets initiative (SBTi) can reinforce that ambition by:

- anchoring targets in scientific scenarios;

- increasing external credibility;

- increasing comparability within the sector.

Dimension 3: climate transition plan and decarbonisation

A climate transition plan translates objectives into a coherent framework of measures, investments and planning. The technical core of that framework is the decarbonisation plan: the concrete reduction measures that actually reduce emissions. The broader transition plan structures reduction measures, provides insight into the impact of investments, links short- and long-term actions, and integrates climate into strategic planning. Here, choices are made about energy sources, technological innovation, supplier structure and product portfolio.

Dimension 4: climate risk analysis

Climate structurally influences your company's risk profile.

A climate risk analysis provides insight into:

- physical impact (extreme weather conditions, flooding, water stress);

- regulatory developments;

- carbon pricing;

- market shifts;

- the impact of the CBAM on imported materials and products.

An integrated climate risk analysis increases your organisation's resilience and supports informed decision-making.

Dimension 5: Product Carbon Footprint and chain data

Climate impact ultimately manifests itself at product and chain level. Productdata plays a central role in tenders, customer relations and international trade. In light of the CBAM, insight at product level also becomes financially relevant. The Product Carbon Footprint (PCF) quantifies emissions per product, increases transparency towards customers, structures scope 3 data, and ensures reproducible and verifiable calculations. This makes climate visible in your pricing and your position vis-à-vis competitors.

The foundation: clear governance

Climates hould not be a separate, parallel process. A robust climate strategy requires clear anchoring in the organisation and management. Governance ensures that ambition, planning and risk analysis do not exist side by side, but are instead managed coherently. It determines:

- who is responsible for reduction processes;

- how a company monitors progress via KPIs;

- how a company integrates climate into investment and innovation processes;

- how ESG managers, operations, finance and management work together.

Governance thus forms the institutional foundation on which the substantive dimensions rest.

The lever: stakeholder activation

A robust climate strategy cannot succeed without internal and external alignment. Internal activation, supplier engagement, communication with customers and building external credibility: stakeholder involvement is crucial at every step.

Would you like to know how robust your current climate approach is in the face of this external pressure?

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Unordered list

- Item A

- Item B

- Item C

During a targeted half-day intake, we analyse:

After the intake, we will provide you with a clear priority matrix, tailored to your sector and international context.

CSRD-rapportage is geen verslag dat je in enkele maanden tijd realiseert. Het is een organisatiebreed proces dat voorbereiding vraagt op vlak van data, governance, processen en strategie - en dat vergt meer tijd dan de meeste organisaties verwachten.